I have been running hosting infrastructure long enough to remember when "just use AWS" seemed like the obvious answer to every scaling problem. A few years in, customers figured out the egress costs, the lock-in, the proprietary service dependencies that made migration expensive to the point of being theoretical. The lesson was not that AWS was bad—it was that the economics of a platform decision compound quietly until the bill lands and the exit looks impossible.

I am watching the AI inference market set up the same dynamic right now. And Together AI's $800 million Series C, announced July 1, 2026, is the clearest evidence yet that a serious number of operators have decided they are not going to let it happen again.

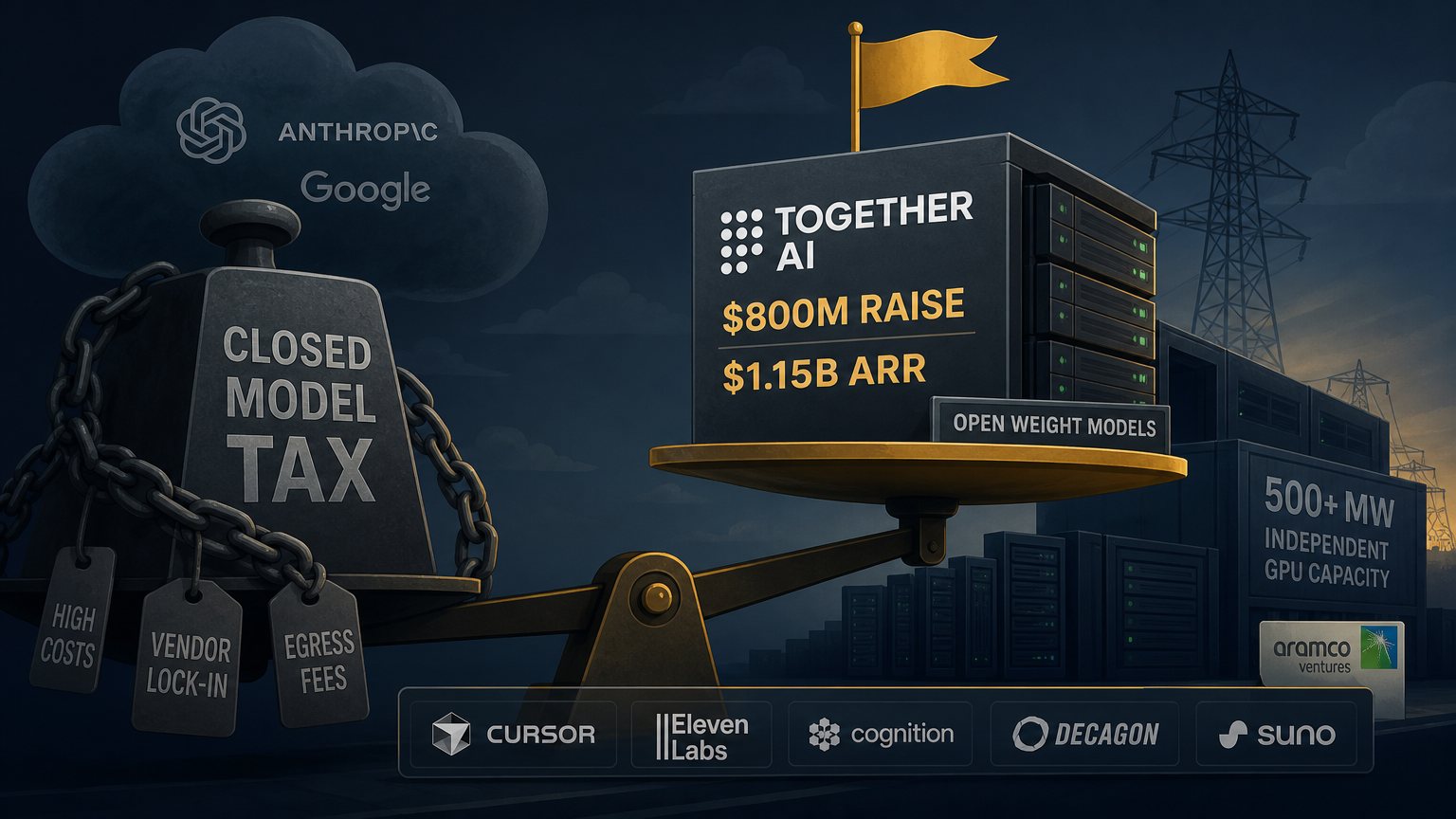

The Numbers That Actually Matter

Together AI closed the round at an $8.3 billion valuation with Aramco Ventures leading, alongside NVIDIA, Vista Equity, General Catalyst, Emergence Capital, Salesforce Ventures, and a dozen others. Those names are interesting but not the signal. The signal is this: the company reported $1.15 billion in annual bookings in Q2 2026.

That is not a projection. That is a run rate. For a company founded in 2022, on a business model that amounts to "let customers run open-weight models on our GPU clusters instead of paying OpenAI or Anthropic," that number says the market for an alternative has arrived.

The round also includes commitments for over 500 megawatts of compute capacity capitalized independently by investors—GPU clusters that Together does not lease from Azure or AWS, but controls directly. That matters for anyone thinking about what "infrastructure independence" actually looks like in the AI era.

What 6× to 20× Actually Means

Together's core pitch is economic. They claim customers running open-weight models through their platform achieve 6x to 20x lower costs compared to closed frontier APIs, while maintaining equal or better performance for their specific workloads. One customer reduced inference costs sixfold after migrating.

The range is wide because the math is workload-specific. For high-volume, repetitive tasks—classification, summarization, extraction, embedding—open-weight models now match or beat closed frontier models on the benchmarks that matter for those tasks. The 87% cost gap between open and closed inference is real, and for any team running production AI at meaningful token volumes, it is not a rounding error.

The industry data backs this up. Analysis from DeepInfra shows that open models achieve roughly 90% of closed-model performance at release, and they close that gap quickly—while costing 87% less to run. Yet per OpenRouter data, closed models from OpenAI, Anthropic, and Google still account for nearly 80% of all AI tokens processed in 2026. The economics clearly favor open weights, but switching cost and inertia are keeping the closed model providers fed.

This is the closed-model tax. Teams are paying it, and most of them know it, and most of them have not changed anything yet.

Together Is Not Just a GPU Rental Shop

What separates Together AI from a commodity GPU cloud is the systems software work. Their recent technical releases include FlashAttention-4 optimized for NVIDIA Blackwell, the Together Megakernel—a fused kernel that reduces operator-level overhead across the inference stack—and together.compile, a compilation toolchain for workload-specific kernel optimization.

This is the kind of low-level infrastructure work that most AI teams cannot afford to do themselves, and that hyperscalers have historically done only for their own proprietary models. When you run DeepSeek, MiniMax, or Llama on Together's platform, you are getting inference performance that has been tuned at the metal level—not just "we have GPUs, bring your weights."

For operators who have tried to self-host open-weight models and hit the gap between "this model benchmarks well" and "this model is fast enough and cheap enough in production," that distinction is not academic. The self-hosting break-even sits around 2 million tokens per day when you factor in infrastructure, engineering time, and operational overhead. Below that threshold, the economics favor managed inference. Above it, self-hosting starts to pencil out—but only if you can do the optimization work. Together is selling the optimization work at a scale most teams cannot match internally.

Who Is Actually Using This

The customer list matters here. Cursor, Eleven Labs, Cognition, Decagon, and Suno are not toy projects. These are companies running AI inference as a core production dependency, at volumes where cost efficiency determines unit economics. When Cursor—whose entire product is AI-assisted coding—chooses an inference provider, they have looked at the numbers hard.

The common thread is workloads where volume is high, latency requirements are moderate, and the specific model capability gap between open and closed is small enough that economics win. For those workloads—which describe a large fraction of real production AI usage—the decision to build on closed frontier APIs looks increasingly like the AWS egress mistake replayed.

The Aramco Angle Deserves a Second Look

Aramco Ventures leading this round is not the strange choice it might appear. Saudi Aramco is one of the largest energy companies in the world, and AI compute is an energy business. A 500-megawatt GPU cluster runs on power—a lot of it. For an energy producer, investing in the infrastructure that will consume an increasingly large share of global electricity output is a direct play on demand for their product.

This is the same logic that drives National Grid's investments in data center-adjacent generation capacity. The inference infrastructure buildout and the energy industry are not separate stories. They are the same capital flowing in both directions. When Aramco writes an $800 million check to an AI inference company, they are partially investing in their own future customers.

For infrastructure operators, this means the major commodity providers—energy, networking, compute—are increasingly integrated into the AI stack. Vendor dependencies in AI infrastructure now go deeper than model APIs.

What This Means If You Run AI in Production

The practical question is where your team sits relative to the economics. A few things are now clearer than they were a year ago:

- The performance gap is small and shrinking. For most production workloads outside of complex multi-step reasoning, open-weight models on optimized inference infrastructure match closed-model performance. The benchmark gap that justified paying the closed-model premium in 2024 is largely gone for the workloads that generate volume.

- The cost gap is not small. 6x to 20x is not a marginal efficiency. At scale, this is the difference between an AI product with healthy unit economics and one that is fundamentally unviable without venture subsidy.

- Managed open-weight inference is now a mature infrastructure category. Together AI at $1.15 billion ARR is not an experiment. It is a production infrastructure provider with enough scale to invest seriously in the systems software layer.

- The lock-in question is different, not absent. Switching from OpenAI to Together AI does reduce vendor lock-in on the model side—you can take your weights elsewhere. But it adds infrastructure dependency on Together. The portability argument is strongest if you are running open weights on infrastructure you control, which brings the self-hosting economics back into view for high-volume workloads.

The teams I respect most right now are running a deliberate split: closed frontier APIs for the reasoning-heavy tasks where the capability premium is genuinely worth the cost, and open-weight managed inference for the high-volume automation and retrieval tasks where economics dominate. Analysis of enterprise AI architecture in 2026 describes exactly this pattern emerging at the companies that are getting the unit economics right.

The Bigger Picture

TechCrunch's reporting on the Together AI raise frames this as a neocloud story—a GPU rental company growing up. That framing misses the more important point. What Together AI has proven is that there is a billion-dollar-plus market of operators who have decided that the convenience premium of closed model APIs is not worth the cost and the lock-in. The $800 million raise is not a bet that people want cheaper GPU time. It is a bet that the majority of production AI workloads do not actually need a closed frontier model to get the job done.

That bet is paying off. The teams paying the closed-model tax today will spend the next twelve to eighteen months doing the math and moving workloads. Not all of them—the hardest reasoning tasks will stay on the frontier closed APIs for a while. But a meaningful migration is underway, and Together AI just raised $800 million to be on the right side of it.

I have been in infrastructure long enough to know what it looks like when the economics of a platform decision flip. This is what it looks like.