If you're running production AI systems, you already know: inference isn't free. Every API call, every token generated, every real-time response to a user — it all runs on hardware that someone is paying for. Right now, that hardware is almost universally NVIDIA. H100s, B200s, and whatever comes next. The "NVIDIA tax" is real, and for any organization scaling beyond prototype into production, it shows up fast in your cloud bills.

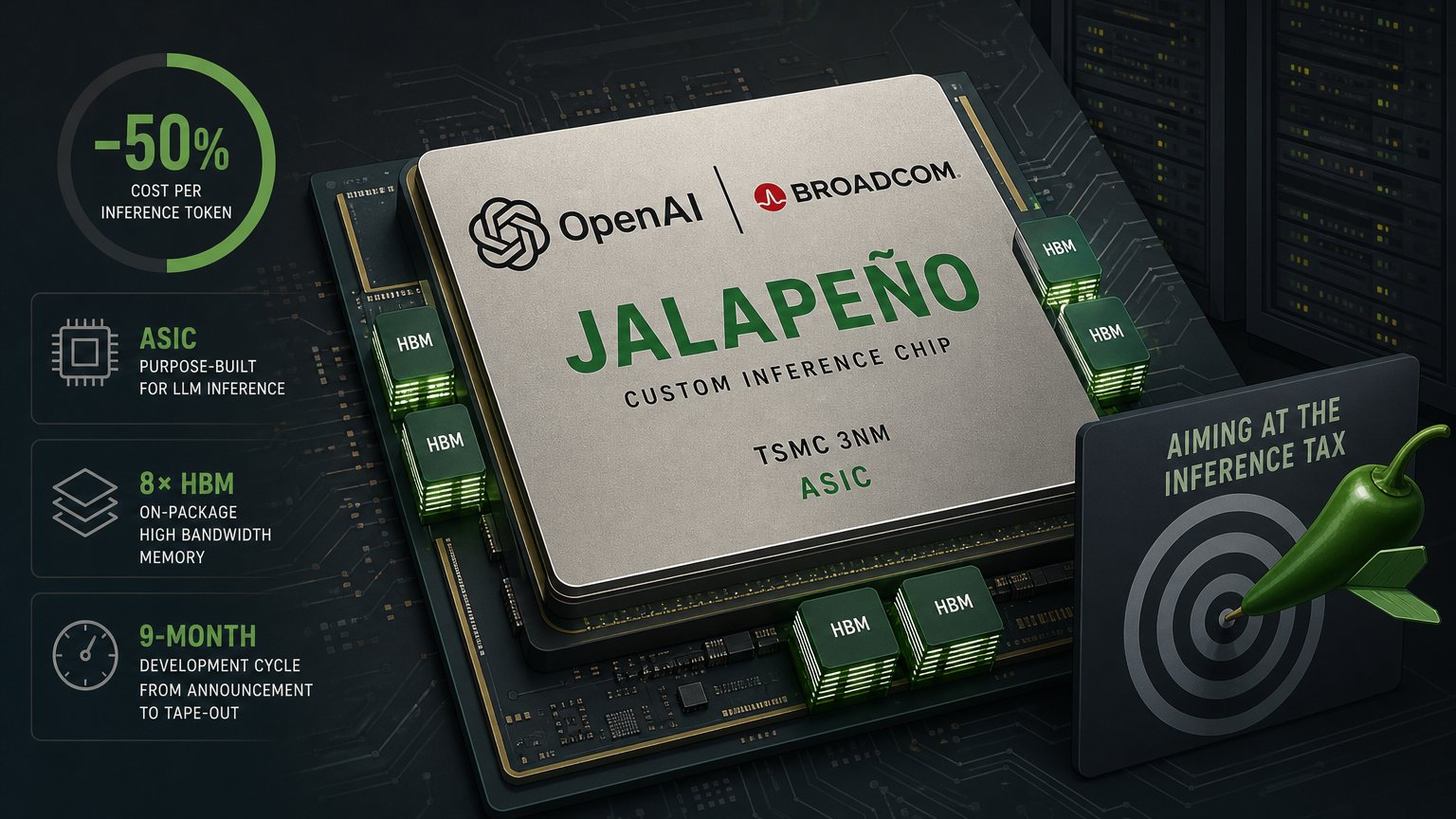

On June 24, 2026, OpenAI and Broadcom announced Jalapeño, OpenAI's first custom inference chip — and the most credible challenge yet to GPU dominance in AI serving. This isn't vaporware. It's a real ASIC built on TSMC's 3nm process, gone from partnership announcement to tape-out in nine months, and targeting small-scale prototype deployments before the end of this year.

The headline performance claim: roughly 50% lower cost per inference token compared to current-generation Nvidia GPUs. If that number holds in production — and that's a big if — it's not an incremental optimization. It's a structural reshaping of what it costs to serve intelligence at scale.

What Jalapeño Actually Is

Jalapeño is an ASIC — an Application-Specific Integrated Circuit. Not a GPU. Not a general-purpose accelerator. A chip designed from first principles around exactly one job: running large language model inference. That distinction matters enormously to how this thing performs.

NVIDIA GPUs are exceptional precisely because they're general-purpose parallel compute engines. That generality is also their inefficiency in this specific use case. When you're running transformer inference, you know ahead of time what operations matter: the memory-movement patterns between attention heads, the kernel shapes that dominate the compute, the networking topology between chips. You don't need floating-point operations optimized for rendering pipelines or scientific simulation. You need something tuned to exactly the memory-bandwidth-to-compute ratio that transformers actually demand.

That's what OpenAI and Broadcom designed for. The architecture centers on a systolic array core — not unlike Google's TPU approach — with eight HBM (High Bandwidth Memory) stacks packaged directly on the die. Stacking HBM modules on-package rather than routing through system memory is the right call: it cuts latency and keeps compute elements fed. Memory bandwidth starvation is the dominant bottleneck in LLM serving, not raw FLOPs. An ASIC built around that constraint can dramatically outperform a GPU that wasn't.

The manufacturing process is TSMC 3nm, which puts Jalapeño in the same lithography generation as Apple's M4 and NVIDIA's Blackwell Ultra. This is leading-edge silicon, not a cost-optimized legacy node.

Nine Months from Announcement to Silicon

The partnership between OpenAI and Broadcom was announced in October 2025. Jalapeño was unveiled in June 2026. That's eight months from public announcement to a chip you can actually discuss architecture with — and Broadcom is calling it one of the fastest ASIC development cycles ever achieved at the high-performance end of advanced semiconductors.

I've run infrastructure long enough to have a healthy skepticism of timelines, but I'll give this one credit: it tracks. When you have a clear, well-understood workload — a static inference graph, a fixed set of dominant kernels, a model architecture that hasn't changed fundamentally in years — you can move fast. The hard part of chip design isn't the transistors; it's knowing with certainty what you need the transistors to do. OpenAI has been running GPT-class inference at enormous scale for years. They know exactly what their bottlenecks are.

Greg Brockman, OpenAI's president, put it plainly in the joint announcement: "We have a deep understanding of the workload — how can we build something that will be able to accelerate what's possible?" That's the right question, and the fact that they could answer it in nine months of silicon time says something about how well they understand their own stack.

The Full-Stack Play

What OpenAI is doing with Jalapeño isn't primarily about building a chip. It's about owning the entire inference stack: model architecture, serving software, networking, scheduling, and now the accelerator itself. Google has been doing this with TPUs since 2016. Amazon built Trainium for training and Inferentia for inference. Meta has their MTIA chips. Every major AI compute player has come to the same conclusion: if AI inference is your core cost, you cannot afford to cede that layer to a third party.

OpenAI is different from those players in one important respect: they're a model company that became an infrastructure company by necessity. They're not AWS. They don't sell compute as a product. But at the scale they're operating — tens of millions of users, real-time API traffic from tens of thousands of enterprise customers — their inference bill is existential. A 50% cost reduction at that scale isn't an optimization. It's a business model change.

This is also why the chip is inference-only. Jalapeño won't run pre-training. NVIDIA retains that workload for now — the irregular, exploratory compute of training frontier models doesn't fit cleanly into a fixed ASIC architecture. But inference is where the dollars are in production. Training happens once per model version; inference happens billions of times per day.

What This Means for Everyone Building on Top

Here's the question I keep coming back to: does any of this flow downstream? If OpenAI's internal compute costs drop by 50%, does that translate into cheaper API pricing for the developers and companies building on top of their models?

The honest answer is: eventually, probably, but not on any predictable timeline. Compute savings at hyperscaler scale rarely map directly onto API pricing. OpenAI will use that margin to fund model development, expand capacity, and compete on capability — not necessarily to drop token prices immediately. That said, infrastructure economics do create pricing floors, and if Anthropic and Google are facing the same ASIC-driven cost compression in their own silicon programs, competitive pressure will push prices down over time. We've already watched API costs fall by an order of magnitude in three years. This is the next driver of that curve.

For teams running significant OpenAI API spend today, I'd treat Jalapeño as a signal about the 2027–2028 cost environment, not a reason to renegotiate your current contracts. Full production ramp is still 12–18 months out, and the prototype deployments at year-end are proofs-of-concept, not fleet replacements.

If you're building AI infrastructure decisions with a three-year horizon — which you should be — this changes the model. The cost of intelligence is going to keep falling. Architecture decisions you make today around cost-based throttling, caching layers, and tier-based model routing should account for a world where that cost may be half of what it is now.

The Competitive Landscape Just Got More Interesting

Broadcom's role in all of this deserves attention. Their AI revenue doubled to $8.4 billion in Q1 2026, driven by custom ASIC work for OpenAI, Anthropic, Meta, and others. Broadcom is quietly becoming the neutral party in a world where everyone wants custom silicon but most organizations don't have the fab relationships or design teams to get there on their own. TSMC does the manufacturing; Broadcom handles the physical design; the model company provides the workload specifications. That three-way structure is likely to repeat across the industry.

NVIDIA isn't going anywhere. Their CUDA ecosystem has a decade of momentum, their software stack is genuinely world-class, and they remain the only real option for training frontier models. But the inference market — where production workloads actually live — is increasingly contested. AMD is making inroads with ROCm. Google's TPUs are available externally. Amazon's Inferentia is in wide use. And now OpenAI's own chip is in the picture.

For infrastructure engineers, the practical takeaway is this: the hardware layer of AI compute is no longer a monoculture. That creates real work — evaluating hardware options, considering cost profiles, potentially managing multi-accelerator serving infrastructure — but it also creates leverage. A market with actual competition is a market where you can negotiate, optimize, and route workloads to the most cost-effective substrate.

Jalapeño is a capable addition to that ecosystem. The nine-month development cycle is legitimately impressive. The 50% cost claim, if it holds in production, is significant. And the signal it sends about OpenAI's infrastructure ambitions is unambiguous: they intend to own the stack from silicon to output token.

I'll be watching the year-end prototype deployment closely. The real story will be in the operational data — power draw per token, failure rates in production, memory bandwidth utilization under real serving load. Those numbers will tell us whether Jalapeño delivers on its promise, and whether the inference economics shift that OpenAI is betting on actually becomes real.