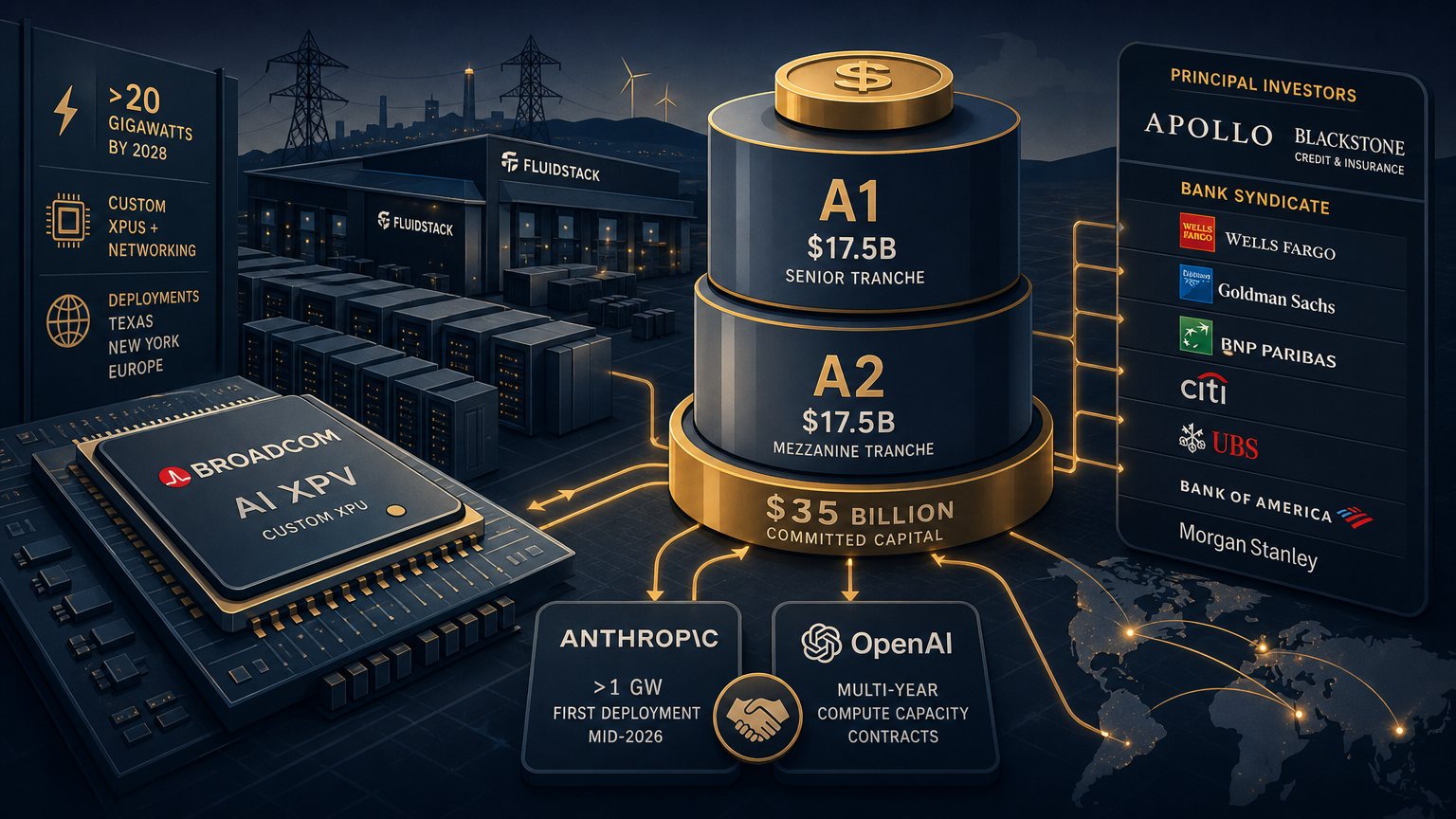

The numbers from the June 9th announcement are the kind that require a second read. Thirty-five billion dollars. Twenty-plus gigawatts. A financing structure coordinated across Apollo, Blackstone, Wells Fargo, Goldman Sachs, BNP Paribas, Citi, UBS, Bank of America, and Morgan Stanley — all organized around a single semiconductor company's custom chip platform. The Broadcom AI XPV Platform, announced June 9, 2026, is a lot of things at once: a capital markets transaction, a silicon bet, a sovereign infrastructure play, and a restructuring of how frontier AI compute gets funded. I want to work through what it actually means, because the headline numbers are almost distracting from the more interesting story underneath them.

What the Platform Actually Is

Strip away the financial jargon and the structure is clear. Broadcom supplies custom XPUs — application-specific integrated circuits designed for AI training and inference — along with optimized networking. Apollo leads the financing as principal investor, backed by Blackstone's Credit and Insurance business and a syndicate of global banks. Frontier AI labs, starting with Anthropic and including OpenAI, sign multi-year contracts for dedicated compute capacity. The financing wraps around those contracted cash flows, treating them the way infrastructure investors treat power purchase agreements or toll road revenues: long-dated, predictable, mission-critical.

The initial tranche is $35 billion, structured in two layers (A1 and A2) with separate bank syndicates. The first deployment is Anthropic's capacity expansion — more than one gigawatt of compute, deploying at Fluidstack-based sites in Texas and New York starting mid-2026. The platform targets over 20 gigawatts in total capacity by 2028.

To put 20 gigawatts in context: global data center peak power demand was approximately 104 gigawatts worldwide in 2025, projected to reach roughly 132 gigawatts by the end of 2026. This single platform is targeting capacity equivalent to roughly 15 percent of current global data center power demand — not as a hyperscaler's internal buildout, but as a purpose-built AI compute vehicle financed by private credit.

Why Private Credit, and Why Now

The financing structure is the part I find most technically interesting, and it's receiving less attention than it deserves. Apollo isn't a lender in the traditional sense here — they're acting as a principal investor committing capital through their High-Grade Capital Solutions, Apollo Capital Solutions, and ATLAS SP Partners platforms. The press language is deliberate: "committed, certain capital across a multi-year draw schedule" for infrastructure with "contracted cash flows, mission-critical utility."

That language mirrors how institutional investors talk about regulated utilities, fiber networks, and power generation — not technology companies. Apollo and Blackstone together manage north of $2.3 trillion in assets. What they're doing is applying an infrastructure investment framework to compute silicon, which has historically been too fast-moving and too illiquid to attract this kind of patient capital.

The XPV Platform works because two things converged. First, AI compute at scale now behaves like utility infrastructure: large customers need capacity years in advance, they sign multi-year contracts, and the switching costs are substantial enough that the revenue is genuinely predictable. Second, Broadcom's XPU technology offers something frontier AI labs can't easily get elsewhere — custom ASICs designed around specific model architectures, promising lower per-token costs and better power efficiency than general-purpose GPUs. That technical moat is what makes the long-term contracts credible and the private credit terms achievable.

The Custom Silicon Argument

I've been watching the ASIC versus GPU debate for several years, and I think most people still underweight the ASIC side. Nvidia's dominance in AI training was built on the CUDA ecosystem and the flexibility of general-purpose GPUs — if you didn't know exactly what workloads you'd run, GPUs were the only rational answer. At startup scale and mid-market, that flexibility still matters enormously.

But at gigawatt-class scale — training runs that consume hundreds of megawatts, inference serving at hundreds of millions of daily active users — the economics shift. Power efficiency and per-token cost start to dominate the decision matrix in a way they don't when you're renting a hundred A100s for a fine-tuning job. A custom ASIC designed for a specific model family, with optimized memory bandwidth and interconnect topology, can beat a general-purpose GPU on those metrics by a significant margin.

Broadcom has quietly built a strong track record here. They supply custom silicon for Google's TPU program and have production engagements with multiple hyperscalers. The XPV Platform is a strategic bet that this capability — custom silicon paired with the capital structure to deploy it at scale — can become a durable franchise through 2028 and beyond. For Anthropic and OpenAI, trading some hardware flexibility for capacity certainty and better per-token economics is rational when your compute needs are predictable at multi-gigawatt scale anyway.

What This Means If You Run Real Infrastructure

Three practical implications for people who run systems rather than invest in them:

Power availability is tightening faster than the headline numbers suggest. Global data center electricity consumption grew 17 percent in 2025 and Gartner projects another 26 percent increase in 2026. The IEA has flagged that bottlenecks are already driving a scramble for solutions. When a single platform commits to 20 gigawatts by 2028, those commitments translate into power purchase agreements and utility contracts in specific markets — Northern Virginia, Texas, New York, and emerging European corridors — that reduce what's available to everyone else. If you're planning data center expansions for 2027 or 2028, your power procurement timeline needs to move now.

The Fluidstack deployment model is worth understanding. Anthropic isn't building traditional data centers here — they're deploying into Fluidstack-operated facilities. Fluidstack runs a hybrid model: a marketplace aggregating third-party GPU capacity and a private cloud segment where it directly owns and operates infrastructure, currently managing over 100,000 GPUs. The pattern — purpose-built facilities operated by a specialist provider under long-term compute contracts, with financing and silicon layers owned separately — is becoming a template. It decouples financing (Apollo/Blackstone), silicon (Broadcom), and operations (Fluidstack) in a way that's more modular than hyperscaler-owned infrastructure.

General-purpose cloud compute and frontier AI compute are diverging. AWS, Azure, and Google Cloud remain the right answer for the vast majority of workloads. But the most cost-efficient frontier compute is increasingly going to purpose-built infrastructure that isn't available on the public spot market. Organizations that need to train large models or run high-volume inference at scale should think about their capacity strategy the way they think about power procurement: long-term contracts, not on-demand pricing, are going to define access to the best hardware.

The Broader Pattern

The XPV Platform didn't emerge from nowhere. It's the clearest expression of a shift that's been building since 2024: AI infrastructure has become too capital-intensive and too strategically important to live on normal technology balance sheets. OpenAI's Stargate program targets ten gigawatts. China has committed $295 billion to data center buildout. NVIDIA and SK Hynix announced a multi-year co-development partnership this week for next-generation memory tied to AI infrastructure roadmaps. Marvell is joining the S&P 500 on the strength of AI infrastructure demand. The semiconductor and infrastructure layers of AI are becoming a financial asset class, not just a technology procurement category.

Broadcom CEO Hock Tan called June 9th "a historic inflection point." Executive quotes in press releases are usually hollow. This one earns it. The financing model for AI compute changed on Monday, and the change is structural. Private credit with infrastructure-style terms, secured against contracted AI compute revenues, will attract hundreds of billions of dollars in institutional capital over the next decade. Organizations that understand this shift — and adjust their capacity planning, power procurement, and vendor relationships accordingly — will be in a materially better position than those who don't. The XPV Platform is the signal. Take it seriously.